Common Product Structures in Consumer Finance

Date: October 2024

Last Update: October 2024

Consideration of Product Structures

Financial products require a careful balance between business volume (revenue) and risk (cost) from inception, which differs from typical consumer products where business models can be optimized post-launch. Establishing the right product structure is fundamental to credit business sustainability. This is particularly important because financial products have universal appeal when perceived as “free money,” yet their structure - including repayment frequency and maturity - directly impacts customers’ ability and likelihood to repay. Therefore, thoughtful product design that aligns business objectives with risk management is essential from the start.

When evaluating product structures, I consider the following key dimensions:

Use Case and Acquisition Channels (Frontend): The primary use case defines both the target user segment and user quality. Understanding this is critical for product positioning.

Limit and Limit Type (Backend; Risk Management): These parameters determine risk exposure levels and should align closely with the intended use case.

Repayment Plan (Backend; Risk Management): The maturity period and repayment frequency significantly influence customer repayment behavior and must be carefully structured.

Collateral (Backend; Risk Management): The presence of collateral or required down payments can effectively mitigate risk exposure.

Interest Rate and Fees (Frontend and Backend; Target User and Risk Management): Interest rates not only define the target customer segment but also establish the acceptable margin of error for risk management.

Comparison of Consumer Finance Products

Characteristics |

Credit Card (Revolving) |

Credit Card Installment Plans |

Buy Now Pay Later (BNPL) |

Peer-to-Peer (P2P) Lending |

Payday Loan |

Pay in 4 |

56 Loan (Philippines); 9出13归 (Hong Kong) |

Auto Title Loans |

Store Credit Cards |

Personal Loans |

Secured Personal Loans |

|---|---|---|---|---|---|---|---|---|---|---|---|

Source of Fund |

Issuing Bank |

Issuing Bank |

Fintech Companies, Merchants |

Individual Investors via Online Platforms |

Non-Bank Financial Institutions |

Fintech Companies, Merchants |

Non-Bank Financial Institutions |

Specialized Lenders |

Retailers/Financial Partners |

Banks, Credit Unions, Online Lenders |

Banks, Credit Unions |

Limit Type |

Revolving |

Instalment |

Instalment |

Term Loan |

Term Loan |

Instalment |

Instalment |

Term Loan |

Revolving |

Term Loan |

Term Loan |

Repayment Frequency |

Monthly |

Monthly |

Bi-weekly/Monthly |

Monthly |

Single Payment |

Initial + Bi-weekly |

Weekly/Bi-weekly |

Monthly |

Monthly |

Monthly |

Monthly |

Repayment Maturity |

Revolving (no fixed end date) |

Short to Medium-term |

Short-term (weeks to months) |

Short to Medium-term |

Very Short-term (1-4 weeks) |

6 weeks |

Short-term (1-3 months) |

Short to Medium-term |

Revolving (no fixed end date) |

Medium to Long-term |

Medium to Long-term |

Repayment Payment |

Minimum monthly payment |

Fixed Monthly Payments |

Equal installment payments |

Fixed Monthly Payments |

Lump Sum Payment |

4 Equal Payments (1 upfront + 3 bi-weekly) |

Fixed Payments |

Fixed Monthly Payments |

Minimum Monthly Payment |

Fixed Monthly Payments |

Fixed Monthly Payments |

Secured or Unsecured |

Unsecured |

Unsecured |

Unsecured |

Unsecured or Secured |

Unsecured |

Unsecured |

Unsecured |

Secured (Vehicle) |

Unsecured |

Unsecured or Secured |

Secured |

Interest Rate and Fees |

Interest Rate: High |

Interest Rate: Moderate |

Interest Rate: Zero to Moderate |

Interest Rate: Moderate |

Interest Rate: Very High |

Interest Rate: Usually Zero |

Interest Rate: Very High |

Interest Rate: High |

Interest Rate: High |

Interest Rate: Low to Moderate |

Interest Rate: Low |

Use Cases |

Everyday purchases, Building credit |

Large purchases, Budget Management |

Online shopping, Retail purchases |

Personal Loans, Debt Consolidation |

Emergency Expenses |

Online Shopping, Small-Medium Purchases |

Emergency Expenses |

Emergency Expenses |

Store-specific Purchases |

Large Purchases, Debt Consolidation |

Large Purchases, Debt Consolidation |

Sales Channel |

Online, Bank Branches, Retail Partners |

Online, Bank Branches, Retail Partners |

E-commerce Platforms, Retail Stores |

Online P2P Platforms |

Online, Physical Stores |

E-commerce Sites, Retail Partners |

Online, Physical Stores |

Physical Stores |

Retail Stores, Online |

Online, Bank Branches |

Bank Branches, Online |

Supplementary Notes on Credit Card Model

Three-Party vs Four-Party Credit Card Models

The credit card industry operates primarily under two main models: the three-party model (closed loop) and the four-party model (open loop).

Three-Party Model (Closed Loop)

In a three-party model, the key parties are:

The cardholder (consumer)

The merchant

The card issuer/network (single entity)

Examples include American Express and Discover, where the company acts as both the card issuer and payment network. Key characteristics:

Direct relationships with both cardholders and merchants

Full control over fees and terms

Typically higher merchant fees but also higher cardholder rewards

More integrated customer experience

Limited acceptance compared to four-party networks

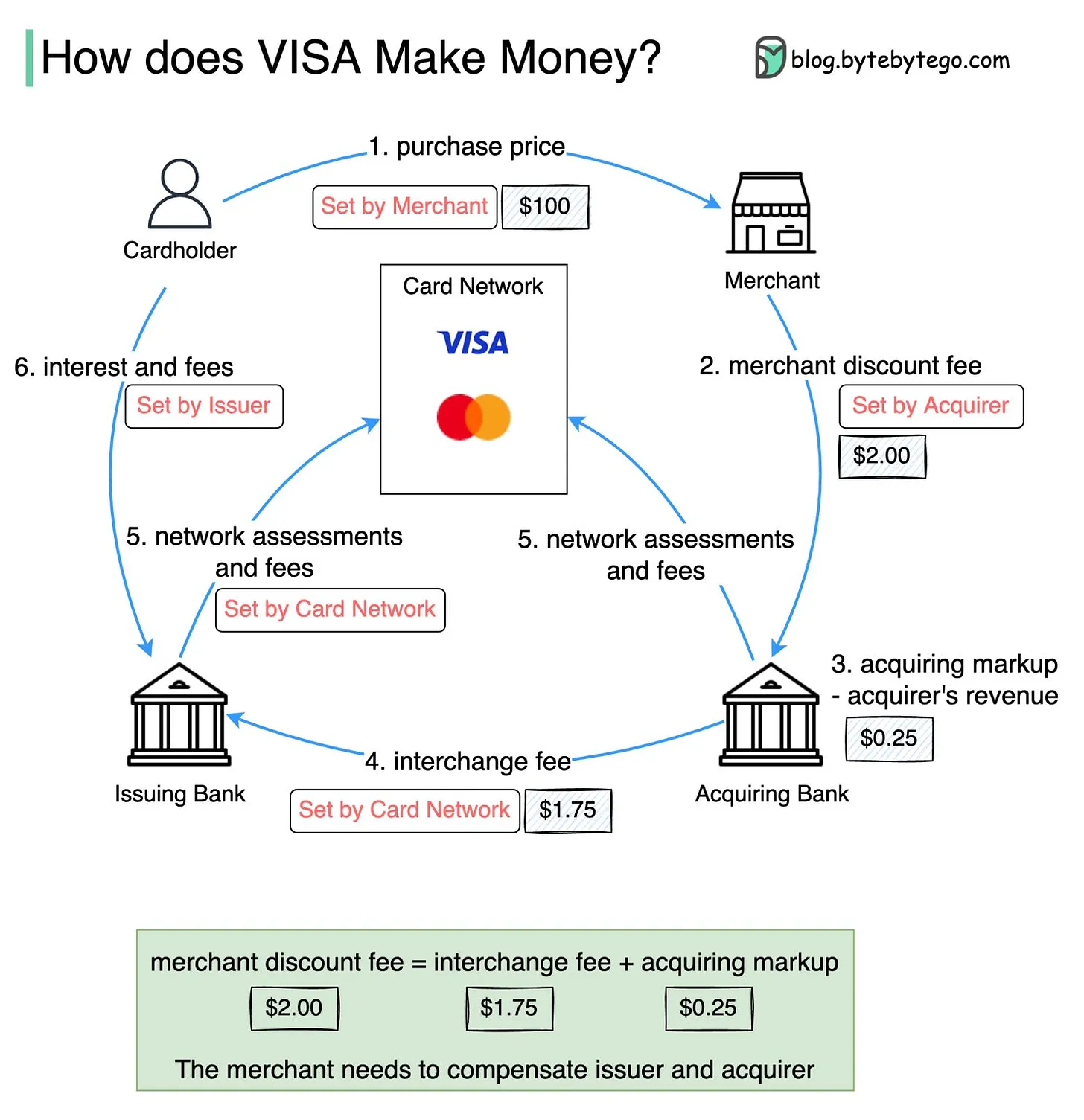

Four-Party Model (Open Loop)

In a four-party model, the participants are:

The cardholder (consumer)

The merchant

The issuing bank

The acquiring bank/payment network

Examples include Visa and Mastercard networks. Key characteristics:

Broader merchant acceptance

Shared revenue and risks among participants

More complex fee structure

Greater competition among issuers

Network effects benefit all participants